|

|

Abstract

It is known that an adaptation of Newton's method allows for the computation of functional inverses of formal power series. We show that it is possible to successfully use a similar algorithm in a fairly general analytical framework. This is well suited for functions that are highly tangent to identity and that can be expanded with respect to asymptotic scales of “exp-log functions”. We next apply our algorithm to various well-known functions coming from the world of quantitative finance. In particular, we deduce asymptotic expansions for the inverses of the Gaussian and the Black–Scholes pricing functions.

Keywords: Asymptotic expansion, algorithm, pricing, Hardy field, exp-log function, Black–Scholes formula

One notoriously complex problem in finance is the pricing of derivative products that are frequently traded on financial markets. Practitioners have proposed various sophisticated models for the dynamics of financial assets. In particular, it has been necessary to account for the existence of U-shaped “volatility smiles” which play a central role in the pricing of so-called vanilla options. Some models seem more reasonable than others because they explain not only the volatility smile, but also have properties that are directly exploitable in practice, notably the existence of easily implementable pricing formulas involving mathematical parameters that are easy to calibrate.

Subsequently, the volatility smile has been studied in a fairly general way, with a minimum of hypotheses on the probabilistic distribution of the assets [3, 4, 8, 16, 25]. This has made it possible to isolate intrinsic behaviours that are shared by a large number of models in the study of volatility smiles.

The next step has been to study the volatility smile in a model-free setting. This ultimately leads to focusing not on the Black–Scholes formula itself but on its inverse [10, 14, 30, 36]. A notable advantage of this approach is that it simplifies pricing problems. Indeed, in the case of vanilla options, such problems usually do not admit closed form solutions (except in the Black–Scholes model), so we need to resort to approximate solutions. Different techniques have been proposed to this purpose: perturbation methods with partial or stochastic differential equations, Lie symmetry theory, Watanabe theory, heat kernel expansion theory and Minakshisundaran–Pleijel's formula, large deviation theory, etc. [7, 12, 17, 20, 26, 27]. Most of these techniques give the asymptotics of price for large or small values of certain parameters involved in the computation of option prices. The study of the inverse function of the Black–Scholes formula then transforms vanilla option price asymptotics into implicit volatility asymptotics, which is the quantity of interest.

The problem of inverting Black–Scholes formula is challenging because of its non-analytic boundary behaviour. In fact, since the Black–Scholes model (as any other stochastic model) uses Brownian motion, it is not surprising that the asymptotics of the Black-Scholes formula involves logarithms. More precisely, after a suitable change of variables, the relation between vanilla option price and volatility can be expressed via an asymptotic expansion

where  are polynomials in

are polynomials in  [10, 14]. In particular, this means that

[10, 14]. In particular, this means that

for every  . We are interested

in computing a similar expansion for

. We are interested

in computing a similar expansion for  in terms of

in terms of

.

.

In computer algebra, various techniques have been developed for

asymptotic expansions in general asymptotic scales. For instance,

several algorithms exist for the asymptotic expansion of

“exp-log” functions [15, 22, 29, 34, 35]. Such functions are

built up from the rationals and an infinitely large variable  using the field operations, exponentiation and logarithm.

An example of an exp-log function is

using the field operations, exponentiation and logarithm.

An example of an exp-log function is  .

The theory of transseries [9, 21, 23]

makes it possible to cover asymptotic expansions of an even wider class

of functions comprising many formal solutions to non-linear differential

equations.

.

The theory of transseries [9, 21, 23]

makes it possible to cover asymptotic expansions of an even wider class

of functions comprising many formal solutions to non-linear differential

equations.

Several algorithms also exist for the functional inversion of exp-log

functions [32, 33]. However, the right-hand

side  of (1) is usually not an

exp-log function, so these algorithms cannot be applied directly. When

considering

of (1) is usually not an

exp-log function, so these algorithms cannot be applied directly. When

considering  as a formal transseries, there are

also methods for computing the formal inverse

as a formal transseries, there are

also methods for computing the formal inverse  of

of

[21, 23]. However,

a priori, the analytic meaning (2) is lost during

such formal computations. In this paper, we will show how to invert

asymptotic expansions of the form (1) from the analytic

point of view.

[21, 23]. However,

a priori, the analytic meaning (2) is lost during

such formal computations. In this paper, we will show how to invert

asymptotic expansions of the form (1) from the analytic

point of view.

For each , let  be the ring of

be the ring of  -fold

continuously differentiable functions at infinity (

-fold

continuously differentiable functions at infinity ( ). Then

). Then  is a

differential ring. We recall that a Hardy field is a

differential subfield

is a

differential ring. We recall that a Hardy field is a

differential subfield  of

of  . It is well-known that Hardy fields [5,

18, 19] provide a suitable setting for

asymptotic analysis. In section 2, we will introduce the

abstract notion of an “effective Hardy field”, which

formalizes what we need in order to make this asymptotic calculus fully

effective. Typical examples of effective Hardy fields are generated by

exp-log functions. For instance, in Sections 2.3 and 2.4, we will show that

. It is well-known that Hardy fields [5,

18, 19] provide a suitable setting for

asymptotic analysis. In section 2, we will introduce the

abstract notion of an “effective Hardy field”, which

formalizes what we need in order to make this asymptotic calculus fully

effective. Typical examples of effective Hardy fields are generated by

exp-log functions. For instance, in Sections 2.3 and 2.4, we will show that  is effective

Hardy field. Using the aforementioned work on expansions of exp-log

functions, it is possible to construct various other effective Hardy

fields.

is effective

Hardy field. Using the aforementioned work on expansions of exp-log

functions, it is possible to construct various other effective Hardy

fields.

Let be a Hardy field. We say that  with

with  is steep if for any

is steep if for any

, there exists a

, there exists a  with

with  . An

element is said to be highly tangent to

identity if there exists a

. An

element is said to be highly tangent to

identity if there exists a  with

with  . For instance, if

. For instance, if  , then

, then  is steep and

is steep and

is highly tangent to identity, contrary to

is highly tangent to identity, contrary to  . Now assume that

is an effective Hardy field. We say that a germ

. Now assume that

is an effective Hardy field. We say that a germ  admits an effective asymptotic expansion over if

for every we can compute an element

admits an effective asymptotic expansion over if

for every we can compute an element  with

with  . If

. If  is highly tangent to identity and

is highly tangent to identity and  , then we will prove in Section 3

that

, then we will prove in Section 3

that  admits a functional inverse that also

admits an effective asymptotic expansion over . Applied to the case when , this gives an algorithm for inverting asymptotic

expansions of the form (1). Our algorithm relies on two

main ingredients: Taylor's formula for right composition with functions

that are highly tangent to identity, and Newton's method for reducing

functional inversion to functional composition.

admits a functional inverse that also

admits an effective asymptotic expansion over . Applied to the case when , this gives an algorithm for inverting asymptotic

expansions of the form (1). Our algorithm relies on two

main ingredients: Taylor's formula for right composition with functions

that are highly tangent to identity, and Newton's method for reducing

functional inversion to functional composition.

For our application to mathematical finance, it would have sufficed to

work with the particular effective Hardy field . There are several reasons why we have chosen to

prove our main result for general effective Hardy fields. First of all,

the more general result may be useful in other areas such as

combinatorics [31]. Indeed, functional inverses frequently

occur when analyzing asymptotic behavior using the saddle point method.

Secondly, our general setup only requires a moderate

“investment” in the terminology from Section 2.

Finally, it is natural to prove the results from Section 3

in this setup; the proofs would not become substantially shorter in the

special case when .

This paper contains three main contributions. As far as we are aware, the application of modern asymptotic expansion algorithms to mathematical finance is new. Secondly, we introduce the framework of effective Hardy fields which we believe to be of general interest for effective asymptotic analysis. One major advantage of this framework is that it separates the potentially difficult question of constructing a suitable effective Hardy field from its actual use. The existing literature on exp-log functions and transseries can be put to use for such constructions. But for various other problems, it suffices to assume the effective Hardy field to be given as a blackbox. The third contribution of this paper is to show that this is particularly the case for the inversion of asymptotic expansions that are “highly tangent to identity”.

Acknowledgment. We are very grateful to Martino Grasselli for his encouragement and for the careful reading of our work.

Consider the differential ring ,

where denotes the ring of -fold continuously differentiable functions at

infinity () for each . We recall that a Hardy

field is a differential subfield of . Since any non zero element of Hardy fields is invertible, the sign of  is ultimately constant for .

We define

is ultimately constant for .

We define  if is

ultimately positive. It can be shown that this gives

the structure of an ordered field.

if is

ultimately positive. It can be shown that this gives

the structure of an ordered field.

The well-known asymptotic relations  ,

,

,

,  and

and

can be defined in terms of the ordering on : given

can be defined in terms of the ordering on : given  , we write

, we write

and

The quasi-ordering is total on  : given

: given  ,

we have

,

we have  .

.

Example  of exp-log germs at infinity is the smallest

subset of

of exp-log germs at infinity is the smallest

subset of  that contains

that contains  and the identity function, and which is closed under

and the identity function, and which is closed under  ,

,  ,

,

,

,  ,

,  and

and  . For instance,

. For instance,  .

In his founding work [18, 19], Hardy showed

that forms a Hardy field.

.

In his founding work [18, 19], Hardy showed

that forms a Hardy field.

Example  , its Liouville

closure

, its Liouville

closure  is the smallest subset of that contains and that is stable

under , , ,

, , and integration. It is

well known that is again a Hardy field [5].

is the smallest subset of that contains and that is stable

under , , ,

, , and integration. It is

well known that is again a Hardy field [5].

Let be a Hardy field. Given , let us show that

Let us first assume that  ,

whence

,

whence  , and let

, and let  and

and  be such that

be such that  for all

for all  . Modulo a further

increase of

. Modulo a further

increase of  , we may assume

without loss of generality that the signs of

, we may assume

without loss of generality that the signs of  and

and

are constant for .

Then, for all

are constant for .

Then, for all  , we have

, we have

|

(5) |

Consequently,  for suitable integration constants

for suitable integration constants

. If

. If  , then this yields

, then this yields  .

If

.

If  and

and  ,

then we may take

,

then we may take  in (5), so that

in (5), so that

, and we again obtain . If

, and we again obtain . If  and

, then we clearly have

and

, then we clearly have  . This proves that

. This proves that  , which implies (4). One proves

, which implies (4). One proves

and (3) in a similar way.

and (3) in a similar way.

Let be a Hardy field. We say that is effective if its elements can be represented

by instances of a concrete data structure and if we have algorithms for

carrying out the basic operations  ,

as well as effective tests for the relations

,

as well as effective tests for the relations  ,

,  , and .

, and .

In particular, the effective inequality test for

yields an equality test. Inversely, if we have an algorithm to compute

signs of elements in , then

this yields effective inequality tests for both

and . Similarly, if, given

, we have a way to test

whether  and ,

then this yields effective tests for the relations

and . Indeed, given and

and ,

then this yields effective tests for the relations

and . Indeed, given and  , we have

, we have

and

and  .

.

Example  is an effective Hardy field. The basic

operations , , ,

and

is an effective Hardy field. The basic

operations , , ,

and  can clearly be

carried out by algorithm, and it is also clear how to do the equality

test. Now consider

can clearly be

carried out by algorithm, and it is also clear how to do the equality

test. Now consider  with

with  and

and  ,

,  . Then

. Then  .

Consequently,

.

Consequently,  and

and  (resp.

(resp.  ).

).

Example is an effective Hardy field. As above, the

basic operations , , ,

, and

the equality test are straightforward. Now any non zero element  can be written as a fraction

with

can be written as a fraction

with  and ,

. Similarly, we may write

and ,

. Similarly, we may write

with

with  and

and  ,

,  .

Then

.

Then  . Consequently,

. Consequently,  and

and  (resp.

(resp.  ). Here we used the lexicographical

ordering on pairs:

). Here we used the lexicographical

ordering on pairs:  if and only if

if and only if  or

or  and

and  .

.

Example be an effective Hardy field and let  be such that

be such that  and

and  .

Then

.

Then  , whence

, whence  is ultimately strictly increasing and invertible for

composition. Let

is ultimately strictly increasing and invertible for

composition. Let  be the inverse of and assume that

be the inverse of and assume that  .

Then

.

Then  is again an effective Hardy field. Indeed,

since right composition preserves the field operations and the ordering,

is again an effective Hardy field. Indeed,

since right composition preserves the field operations and the ordering,

is effectively isomorphic to

as an ordered field. The derivation on is given

by

is effectively isomorphic to

as an ordered field. The derivation on is given

by  .

.

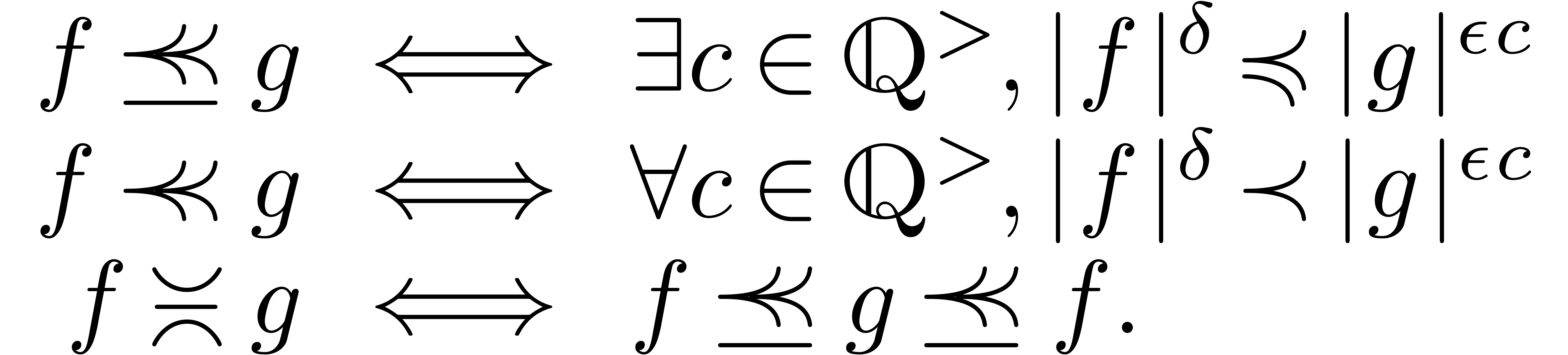

Let and let  be such that

be such that

,

,  . We define the flatness relations

. We define the flatness relations  ,

,  and

and  by

by

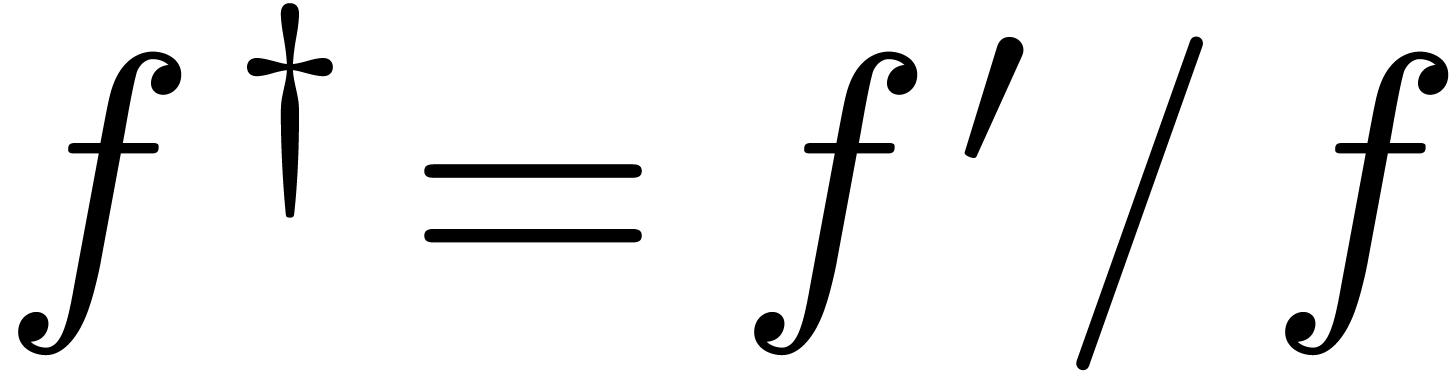

Let  denote the logarithmic derivative of a

function . Taking logarithms,

and using (3) and (4), we observe that

denote the logarithmic derivative of a

function . Taking logarithms,

and using (3) and (4), we observe that

for all and  .

.

An element  is said to be steep if

is said to be steep if  (whence

(whence  )

for all . If

)

for all . If  , then this allows us to define a valuation

with respect to

, then this allows us to define a valuation

with respect to  : we set

: we set  for and

for and  . Notice that the corresponding valuation group

. Notice that the corresponding valuation group

is a subgroup of

is a subgroup of  .

In particular,

.

In particular,  is Archimedean. For and , we notice

that

is Archimedean. For and , we notice

that

Indeed, since and  ,

it suffices to show this for

,

it suffices to show this for  .

Now assume that

.

Now assume that  . Then

. Then  , whence

, whence  for some constant

for some constant  . It

follows that

. It

follows that  . If

. If  , then we also notice that

, then we also notice that  . Indeed,

. Indeed,  and

and  , whence

, whence  .

.

Two examples of steep elements are in  and

and  in . The aim of the remainder of this section is to

generalize Example 4 and prove in particular that is indeed an effective Hardy field.

in . The aim of the remainder of this section is to

generalize Example 4 and prove in particular that is indeed an effective Hardy field.

Let be an effective Hardy field and let  be such that

be such that  for all . By what precedes, this implies

that

for all . By what precedes, this implies

that  for all .

We claim that

for all .

We claim that  is again an effective Hardy field.

Modulo the replacement of

is again an effective Hardy field.

Modulo the replacement of  by

by  (and

(and  by

by  ),

we may assume without loss of generality that

),

we may assume without loss of generality that  and

and  . We clearly have

algorithms for the field operations of

. We clearly have

algorithms for the field operations of  .

Using the rule

.

Using the rule  , it is also

straightforward to compute derivatives of elements of .

, it is also

straightforward to compute derivatives of elements of .

Now consider a polynomial  .

If , then for each

.

If , then for each  , we have

, we have  , so that

, so that  .

Hence implies

.

Hence implies  .

This also shows that

.

This also shows that  , which

provides us with an effective zero test for

, which

provides us with an effective zero test for  , as well as for .

Given a rational function

, as well as for .

Given a rational function  with

and , we also have

with

and , we also have  . Consequently,

and if and only if

. Consequently,

and if and only if  or

or

and

and  .

Similarly, if and only if

or and

.

Similarly, if and only if

or and  .

.

Example as in Example 4, applying the above

argument twice shows that both  and

and  are effective Hardy fields. Applying Example 5

for

are effective Hardy fields. Applying Example 5

for  , we also obtain that

, we also obtain that

is an effective Hardy field.

is an effective Hardy field.

Remark ,

one also needs to show that fields such as  form

effective Hardy fields. One even more difficult problem is to provide an

effective zero test for exp-log constants, i.e. constants

formed from the rationals, using ,

, , , and .

Provided that Schanuel's conjecture holds, such an algorithm was given

by Richardson [28]. His algorithm always returns correct

results, but might not terminate if one explicitly hits a counterexample

to the conjecture. Given a zero-test for exp-log constants, it can be

shown that forms an effective Hardy field [22].

form

effective Hardy fields. One even more difficult problem is to provide an

effective zero test for exp-log constants, i.e. constants

formed from the rationals, using ,

, , , and .

Provided that Schanuel's conjecture holds, such an algorithm was given

by Richardson [28]. His algorithm always returns correct

results, but might not terminate if one explicitly hits a counterexample

to the conjecture. Given a zero-test for exp-log constants, it can be

shown that forms an effective Hardy field [22].

Let be a Hardy field. Given  , there exists a unique

, there exists a unique  with

with  , which is called the

limit of , and

denoted by

, which is called the

limit of , and

denoted by  . We say that is closed under limits if

. We say that is closed under limits if  for all . If

is effective and

for all . If

is effective and  is computable, then we say that

admits an effective limit map.

is computable, then we say that

admits an effective limit map.

An asymptotic scale for is a

multiplicative subgroup  such that

such that  is totally ordered for and such

that there exists a mapping

is totally ordered for and such

that there exists a mapping  with

with  for all . We

call

for all . We

call  the dominant monomial of and notice that

the dominant monomial of and notice that  is necessarily a

group homomorphism. If is effective and is computable, then we call

an effective asymptotic scale.

is necessarily a

group homomorphism. If is effective and is computable, then we call

an effective asymptotic scale.

Assume that is closed under limits and that also admits an asymptotic scale . Given ,

we call  the dominant term of , and notice that

the dominant term of , and notice that  . If and

. If and  are both computable, then the same clearly holds for

are both computable, then the same clearly holds for  .

.

Example  for any

for any  .

This both shows that

.

This both shows that  admits an effective limit

map and that it admits

admits an effective limit

map and that it admits  as an effective

asymptotic scale. Similarly, Example 4 shows that the same

holds for , in which case the

asymptotic scale becomes

as an effective

asymptotic scale. Similarly, Example 4 shows that the same

holds for , in which case the

asymptotic scale becomes  .

.

More generally, let be an effective Hardy field

and let  be as in Section 2.4.

Assume that admits an effective limit map and

that

be as in Section 2.4.

Assume that admits an effective limit map and

that  is an effective asymptotic scale. For each

is an effective asymptotic scale. For each

, we have shown how to

compute an equivalent

, we have shown how to

compute an equivalent  with

and

with

and  . Since

. Since  for any

for any  and

and  ,

the group

,

the group  is totally ordered for

is totally ordered for  . This shows that

. This shows that  admits both an effective limit map and an effective asymptotic scale

.

admits both an effective limit map and an effective asymptotic scale

.

Example

be an effective Hardy field and let be as in

Example 5. If admits an effective

limit map, then so does ,

since  for all .

If admits an effective asymptotic scale , then

admits

for all .

If admits an effective asymptotic scale , then

admits  as an effective asymptotic scale, with

as an effective asymptotic scale, with

for all .

for all .

Let be a Hardy field which contains the identity

function , as well as a steep

element  . If

. If  , then also assume that .

, then also assume that .

An element is said to be highly tangent to

identity if there exists a with . Equivalently, this means that

is of the form  with

with

. If , then this is the case when

. If , then this is the case when  for some

for some  . If , then we rather should have

for some

. If , then we rather should have

for some  . In particular, in

both cases we have

. In particular, in

both cases we have  and even

and even  . We will denote by

. We will denote by  the

subset of of all elements that are highly

tangent to identity.

the

subset of of all elements that are highly

tangent to identity.

Since Hardy fields are not necessarily closed under composition and

functional inversion, the set does not

necessarily form a group. The main aim of this section is to show that a

suitable completion of does form a group

(Theorem 20 below). Moreover, under suitable hypothesis,

there are algorithms for computing asymptotic expansions of compositions

and functional inverses.

Lemma  . Then for any germ

. Then for any germ  with

with  and

and  , we have

, we have

Proof. Without loss of generality, we may assume that

. For any

. For any  , we claim that

, we claim that  .

Indeed, given

.

Indeed, given  , let be such that

, let be such that  has constant sign and

has constant sign and

for .

Assume also that

for .

Assume also that  is defined for . Then

is defined for . Then

for all . We conclude that

, by letting

, by letting  tend to zero.

tend to zero.

The assumption that implies that  , whence

, whence  is strictly

increasing for sufficiently large

is strictly

increasing for sufficiently large  .

This shows that indeed admits an inverse

function

.

This shows that indeed admits an inverse

function  at infinity. Let

at infinity. Let  be such that

be such that  for sufficiently large . Setting

for sufficiently large . Setting  and

and  , our claim implies

, our claim implies

for sufficiently large .

Since is strictly increasing, it follows that

. In other words,

. In other words,  for sufficiently large .

for sufficiently large .

Lemma  and

and  . Then

for any germs

. Then

for any germs  with

with  and

and

, we have

, we have

Proof. Since  is a steep

element, there exists a constant with

is a steep

element, there exists a constant with  . We also notice that

. We also notice that  . Indeed, this is immediate if

. Indeed, this is immediate if  . If

. If  ,

then

,

then  for some

for some  and

and  , since

, since  .

.

Let us first show that  ,

whenever

,

whenever  and

and  .

Since implies

.

Since implies  ,

the function

,

the function  is ultimately decreasing. For

sufficiently large , it

follows that

is ultimately decreasing. For

sufficiently large , it

follows that  for

for  ,

whence

,

whence

Since , this shows that .

Let us next show that we also have in the case

when and  (so that

(so that  ). Then Lemma 10

implies

). Then Lemma 10

implies  , whence

, whence  for some

for some  . Let

. Let

. By what precedes, there

exists an with

. By what precedes, there

exists an with  for all

. Modulo a further increase

of , we may also arrange that

is monotonic for .

It follows that

for all

. Modulo a further increase

of , we may also arrange that

is monotonic for .

It follows that  , whence

, whence

. Post-composing with

. Post-composing with  , we again obtain .

, we again obtain .

Let us finally assume that  .

Then the above arguments prove that

.

Then the above arguments prove that  .

Consequently,

.

Consequently,  .

.

The above arguments conclude the proof in the case when  and

and  . Let us next consider

the case when we still have ,

but is general. Let

. Let us next consider

the case when we still have ,

but is general. Let  be

such that

be

such that  . For sufficiently

large , it follows that

. For sufficiently

large , it follows that  is comprised between

is comprised between  and

and

, which are both equivalent

to . This shows that

, which are both equivalent

to . This shows that  .

.

As to the general case, let  be such that

be such that  . By what precedes, we have

. By what precedes, we have  for all sufficiently large . This shows that

for all sufficiently large . This shows that  .

.

Lemma and  . Let

. Let

and

and  be such that

be such that  and

and  . Then

for any

. Then

for any  with

with  and

and  , we have

, we have

Proof. Let us first consider the case when  and consider

and consider

For sufficiently large ,

Taylor's formula with integral remainder yields

For sufficiently large , the

function  is also monotonic, whence

is also monotonic, whence

By Lemma 11, we have  ,

whence

,

whence  . This completes the

proof in the case when .

. This completes the

proof in the case when .

As to the general case, we have

for all sufficiently large .

Now Lemmas 10 and 11 imply  and similarly

and similarly  . Consequently,

. Consequently,

This concludes the proof in the general case.

Lemma , and

, there exists an with .

, there exists an with .

Proof. Let us first consider the case when , so that  .

For any , we have

.

For any , we have  , whence

, whence  . Consequently,

. Consequently,

It thus suffices to take  in order to ensure that

in order to ensure that

and therefore

and therefore  .

.

Assume next that , so that

. We again have

. We again have  for all , but

this time, we rather obtain

for all , but

this time, we rather obtain  ,

since . Therefore,

,

since . Therefore,

Taking  , we again obtain the

desired result.

, we again obtain the

desired result.

If is an effective Hardy field, then the above

lemmas lead to the following algorithm for approximate composition:

Algorithm compose

,

and with

with

with

Moreover, for all with ,  and

and  , we have

, we have

Let be minimal with

Return

Theorem

Proof. The existence of  is

ensured by Lemma 13. Since is

effective, we have an algorithm for doing the test , which enables us to compute . Setting

is

ensured by Lemma 13. Since is

effective, we have an algorithm for doing the test , which enables us to compute . Setting  ,

our assumption that ensures that . The result now follows from Lemma 12.

,

our assumption that ensures that . The result now follows from Lemma 12.

Remark and , it can be verified that  , that

, that  implies

implies  , and that

, and that  implies

implies  .

.

A well-known way to solve functional equations of the form  is Newton's method [6]. We will now show that

this method indeed yields a quadratic convergence in our setting.

is Newton's method [6]. We will now show that

this method indeed yields a quadratic convergence in our setting.

Lemma  and

and  be such that

be such that  and

and  . Let

. Let  be such that

be such that

Then  .

.

Proof. Since  ,

we notice that

,

we notice that  and

and  .

Let

.

Let  . For all sufficiently

large , we have

. For all sufficiently

large , we have

whence, using the ultimate monotonicity of  on

on

,

,

Using Lemma 11, we also have  and

and

, whence

, whence

Consequently,

Now  implies

implies  and

and  . Consequently,

. Consequently,

This completes the proof.

If is an effective Hardy field, then this lemma

leads to the following algorithm for the computation of approximate

functional inverses:

Algorithm invert

and  with

with

with

Moreover, for any  with

with  and , we have

and , we have

Let

repeat

Let

If  then return

then return

Let

Let

Theorem  . The algorithm

. The algorithm  iterations of the main loop.

iterations of the main loop.

Proof. Let us first show that

throughout the algorithm. This is clear at the start. At each iteration

, Remark 15

implies  and

and  ,

whence

,

whence  , so that

, so that  .

.

On termination, we have  and

and  , whence .

Applying Lemma 10 with

, whence .

Applying Lemma 10 with  and

and  in the roles of

in the roles of  and

and  , we obtain

, we obtain  . Consequently,

. Consequently,  .

Furthermore,

.

Furthermore,  .

.

As to the termination, consider the quantity

At the very start, we have  .

At every iteration

.

At every iteration  , we have

, we have

. Lemma 16

therefore ensures that

. Lemma 16

therefore ensures that  doubles at least, whereas

the algorithm terminates as soon as

doubles at least, whereas

the algorithm terminates as soon as  .

This happens after at most iterations.

.

This happens after at most iterations.

We now extend the definition of high tangency to identity to all germs.

We say that a germ is highly tangent to

identity if there exists a with  and

and  . We denote

by

. We denote

by  the set of such germs. We say that admits an asymptotic expansion over if for every ,

there exists an element with . If we have an algorithm for computing

the set of such germs. We say that admits an asymptotic expansion over if for every ,

there exists an element with . If we have an algorithm for computing  as a function of ,

then we say that admits an effective

asymptotic expansion over .

as a function of ,

then we say that admits an effective

asymptotic expansion over .

Proposition  and

and  admit effective

asymptotic expansions over .

Then so does

admit effective

asymptotic expansions over .

Then so does  . If

. If  , then

, then  .

.

Proof. Given  ,

we may compute and

,

we may compute and  with

with

and

and  .

Assume that there exists an

.

Assume that there exists an  with

with  . Then for all

. Then for all  ,

we must have

,

we must have  and

and  .

Consequently, we may compute

.

Consequently, we may compute  ,

and

,

and  . If

. If  for all , then we also have

for all , then we also have

for all .

for all .

If , then we also get  , whence

, whence  . Moreover,

. Moreover,  ,

whence .

,

whence .

Proposition admits an effective asymptotic expansion over

. Then so does  and

and  .

.

Proof. Given ,

we may compute  with . Let

with . Let  .

Then

.

Then  . Moreover,

. Moreover,  , whence .

, whence .

Combining these two propositions, we have shown the following:

Theorem

that admit

effective asymptotic expansions over forms a

group for functional composition.

that admit

effective asymptotic expansions over forms a

group for functional composition.

function

function

The Lambert function is defined to be the

inverse function of  . Using

our algorithm, we can compute the asymptotic expansion of the inverse

function

. Using

our algorithm, we can compute the asymptotic expansion of the inverse

function  of

of  .

This also yields the asymptotic expansion of

.

This also yields the asymptotic expansion of  for

large .

for

large .

Let  be defined formally by

be defined formally by

and let  be the Gaussian function:

be the Gaussian function:

For any , we have the

well-known relation

where we used the notation

The relation (6) shows that

with  ,

,

|

|

|

|

|

|

|

|

|

|

|

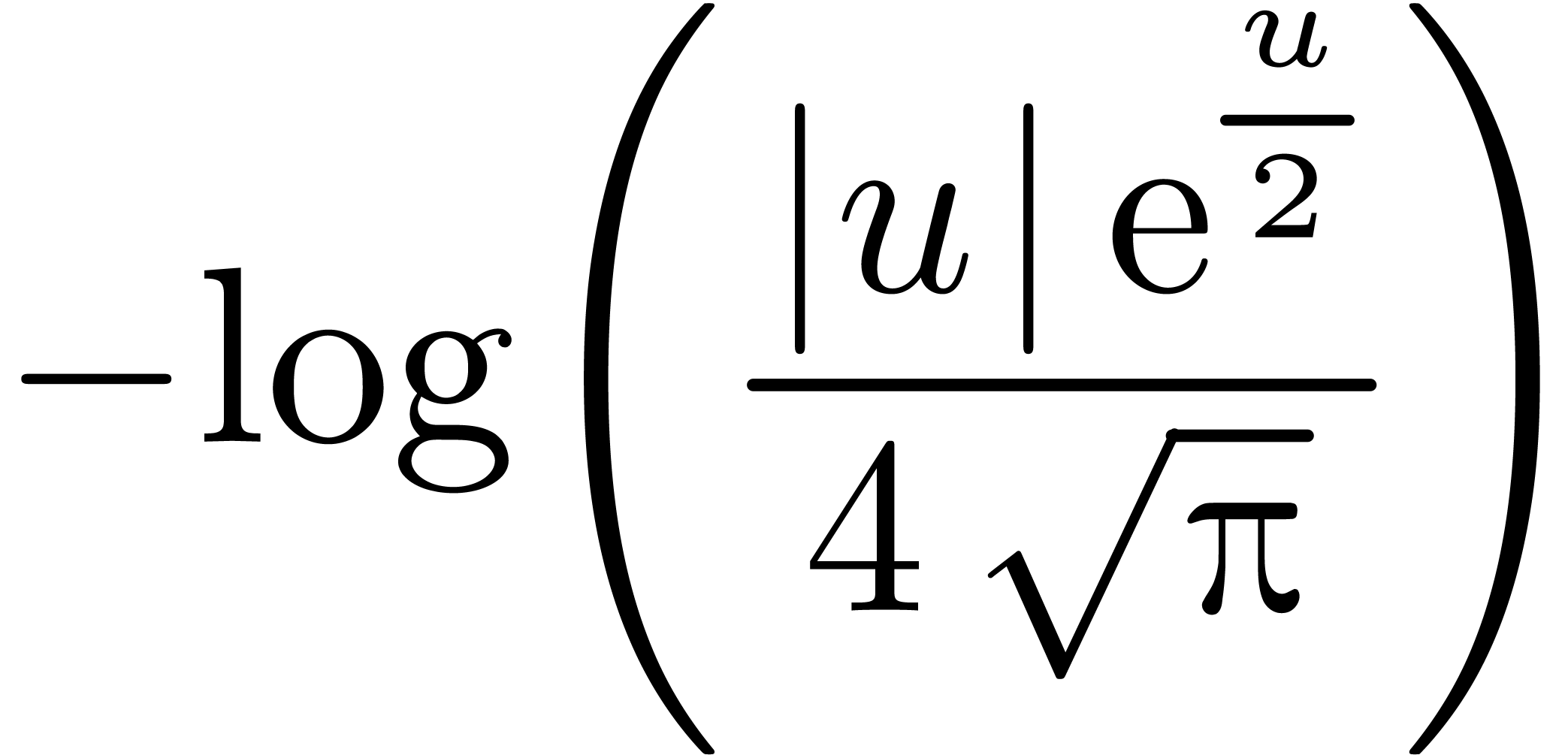

(i>0) |

Our algorithm now allows us to compute the asymptotic expansion of the

inverse function of Gaussian law at  .

This is potentially of great interest in finance when it comes to

calculate risk measures. The formula (7) gives itself an

asymptotic expansion of a Gaussian Value-at-Risk

.

This is potentially of great interest in finance when it comes to

calculate risk measures. The formula (7) gives itself an

asymptotic expansion of a Gaussian Value-at-Risk  in terms of its confidence level

in terms of its confidence level  .

.

The expected shortfall of a portfolio with confidence level  is the expected loss conditional that the loss is greater

than the -th percentile of

the loss distribution. When the return of the portfolio is Gaussian with

mean

is the expected loss conditional that the loss is greater

than the -th percentile of

the loss distribution. When the return of the portfolio is Gaussian with

mean  and volatility

and volatility  , the expected shortfall is

, the expected shortfall is

With  , the relation (6)

yields

, the relation (6)

yields

So, for some constants  , we

have

, we

have

By inverting (7), we get an asymptotic expansion of  in terms of

in terms of  .

.

Let  be defined by

be defined by  and,

for

and,

for  ,

,  . A well-known relation for

. A well-known relation for  tells that for

tells that for  and ,

and ,

Taking logarithms, we get

with  . Considering the CEV

process

. Considering the CEV

process

where is a Brownian motion and  denotes for instance a forward rate, the probability of absorption at

zero before

denotes for instance a forward rate, the probability of absorption at

zero before  -time is given by

-time is given by

Inverting (9) gives a confidence interval where the

probability of absorption of is lower than , asymptotically, for  .

.

By definition, a call option is a contract which gives to the owner the

value  at a future -date

(known today) called maturity of the contract, where

at a future -date

(known today) called maturity of the contract, where  denotes the value at -date

(unknown today) of an asset (like a stock) whose initial value is

denotes the value at -date

(unknown today) of an asset (like a stock) whose initial value is  today, and is a constant

called strike (known today). The initial price of this contract is

denoted by

today, and is a constant

called strike (known today). The initial price of this contract is

denoted by  . In general, by

no-arbitrage arguments, the option price is

always greater than the “intrinsic value”

. In general, by

no-arbitrage arguments, the option price is

always greater than the “intrinsic value”  and lower than the spot value :

and lower than the spot value :

In the Black–Scholes model, the dynamics of  is assumed to be log-normal:

is assumed to be log-normal:

where  is a Brownian motion and

is a constant parameter called volatility. In this framework, the well

known Black–Scholes formula gives the price of any call option. It

can be shown that

is a Brownian motion and

is a constant parameter called volatility. In this framework, the well

known Black–Scholes formula gives the price of any call option. It

can be shown that

where

For simplicity, we have assumed that the interest rate is  . If

. If  are fixed, then it

is easy to see that the function

are fixed, then it

is easy to see that the function

is non-decreasing and one to one from  to

to  . Therefore, in an a

priori non Black–Scholes world and for a given call option

price

. Therefore, in an a

priori non Black–Scholes world and for a given call option

price  observed on the market, there is a unique

solution

observed on the market, there is a unique

solution  (or simply

(or simply  ) of the equation

) of the equation

We call the Black–Scholes implied

volatility associated to and . For different reasons [10, 30], it is interesting to invert the

Black–Scholes function  in (10).

For instance, using techniques from perturbation theory, sophisticated

stochastic models (in a non Black–Scholes world) give only

asymptotic expansions of an option price

in (10).

For instance, using techniques from perturbation theory, sophisticated

stochastic models (in a non Black–Scholes world) give only

asymptotic expansions of an option price  in

terms of the maturity ,

whereas we really need a formula for the implied volatility [4,

20]. Indeed, call option prices are generally quoted in

term of implied volatilities (and not as prices). This can be achieved

in the following manner. In the Black–Scholes model and under the

conditions that

in

terms of the maturity ,

whereas we really need a formula for the implied volatility [4,

20]. Indeed, call option prices are generally quoted in

term of implied volatilities (and not as prices). This can be achieved

in the following manner. In the Black–Scholes model and under the

conditions that  and

and  , it can be proved [14] that the

asymptotic expansion of the “time value”

, it can be proved [14] that the

asymptotic expansion of the “time value”  of the call price

of the call price  , defined

by

, defined

by

is given by

with arbitrarily large,

Therefore, setting

we have

for any integer , where

|

|

|

|

|

|

|

(i>0) |

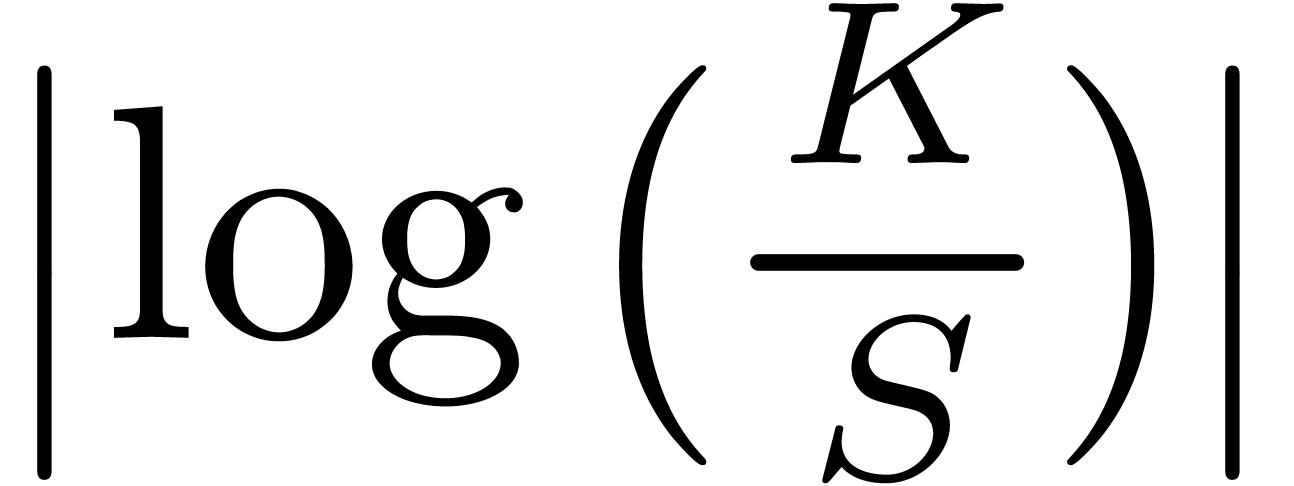

Formula (12) is nothing but another expression for

Black-Scholes formula. Hence we get an asymptotic expansion for  in terms of

in terms of  .

Note that (12) is an asymptotic expansion of a call price

in terms of for large . So, it gives also an asymptotic expansion of a

call price when

.

Note that (12) is an asymptotic expansion of a call price

in terms of for large . So, it gives also an asymptotic expansion of a

call price when  is large i.e. small strike or

large strike.

is large i.e. small strike or

large strike.

Notice also that there is another direct formula  when

when  , which gives an

asymptotic expansion of in terms of

, which gives an

asymptotic expansion of in terms of  .

.

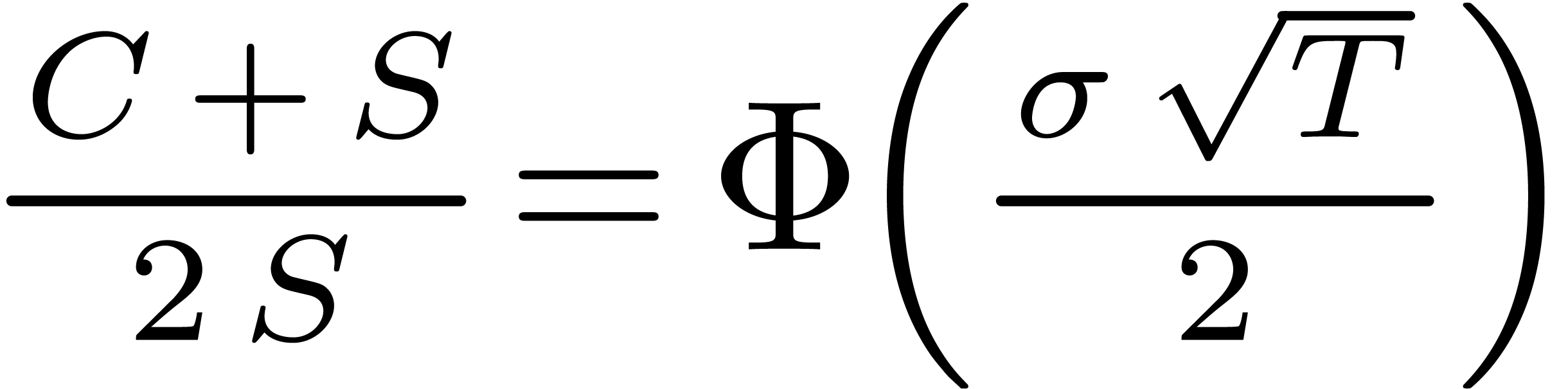

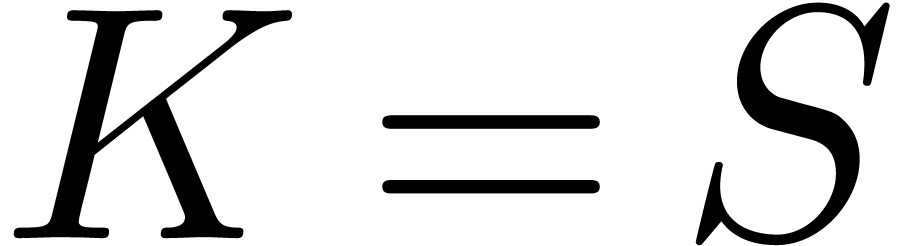

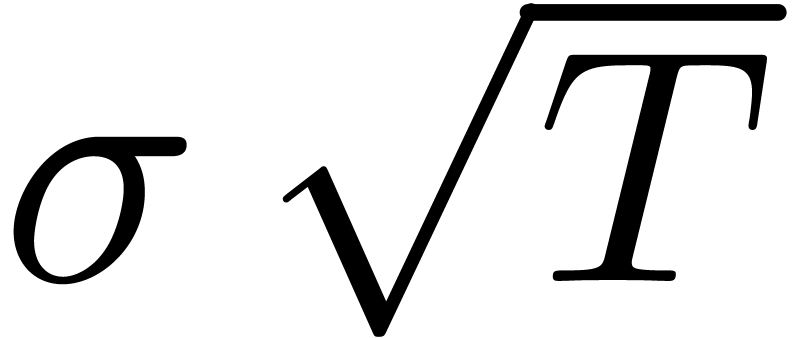

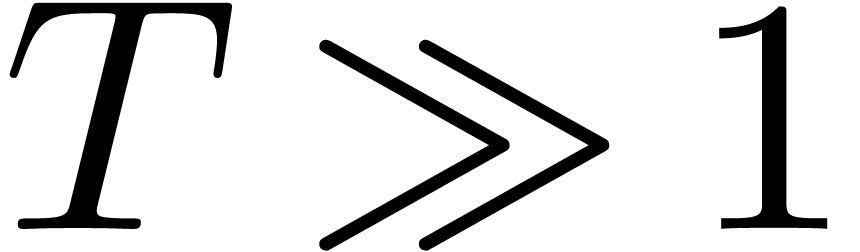

At the limit when  , the first

author previously obtained a similar result [14]. Setting

this time

, the first

author previously obtained a similar result [14]. Setting

this time

and

we have

where

Therefore, we get

where

|

(i>0) |

In the Bachelier model, the dynamics of is

assumed to be normal:

where is a Brownian motion and

is a constant parameter called normal volatility. In this framework, the

price of a call option with strike and expiry is given by Bachelier's

formula

with

Denoting as before by

the time-value of the call option, we have

for  . So, using (8),

we deduce an asymptotic expansion of

. So, using (8),

we deduce an asymptotic expansion of  in terms of

in terms of

for large strike or small maturity in the

Bachelier model. By inverting the Gamma function as before, this gives

an asymptotic expansion of the normal volatility in terms of the

time-value . Therefore, by

comparing with (11), we obtain an equivalence between

normal volatility and lognormal volatility in the cases when or

for large strike or small maturity in the

Bachelier model. By inverting the Gamma function as before, this gives

an asymptotic expansion of the normal volatility in terms of the

time-value . Therefore, by

comparing with (11), we obtain an equivalence between

normal volatility and lognormal volatility in the cases when or  . For

example, when , the first

terms of the expansion are given by

. For

example, when , the first

terms of the expansion are given by

where  denotes the “moneyness”

denotes the “moneyness”  and

and  . Note

that at the money (), we have

a closed form formula [13]:

. Note

that at the money (), we have

a closed form formula [13]:

In particular, taking the derivative in (14) and then

letting gives

where  and

and  are the slopes

of the smiles of volatility at the money:

are the slopes

of the smiles of volatility at the money:

In particular when the volatility smile  is flat

at the money (

is flat

at the money ( ), we have:

), we have:

This is a refinement of a classical result  .

In general, (15) shows that if

.

In general, (15) shows that if  , then the slope of the volatility smile for the

lognormal volatility is negative and this condition holds up to order 1

in [13].

, then the slope of the volatility smile for the

lognormal volatility is negative and this condition holds up to order 1

in [13].

By inverting (12), we get the implied lognormal volatility

from the time-value of

the call-option in a model-free setting. In general, thanks to Tanaka's

theorem, this time-value can be calculated by integrating the density

function of the stochastic process between and

the maturity of the option. On the other hand,

this density function can be obtained using

Minakshisundaram–Pleijel expansion - modulo conditions of

regularity [2]. So, in general this allows to translate an

asymptotic expansion of

from the time-value of

the call-option in a model-free setting. In general, thanks to Tanaka's

theorem, this time-value can be calculated by integrating the density

function of the stochastic process between and

the maturity of the option. On the other hand,

this density function can be obtained using

Minakshisundaram–Pleijel expansion - modulo conditions of

regularity [2]. So, in general this allows to translate an

asymptotic expansion of  for

in an asymptotic expansion of .

for

in an asymptotic expansion of .

As an example, let us consider a local volatility model  . Then Tanaka's formula reads:

. Then Tanaka's formula reads:

In this particular case, the Minakshisundaram–Pleijel expansion gives

with  and

and  is explictly

given by induction [11, 37]. The asymptotic

expansion (17) can be integrated by part and thus give an

asymptotic expansion for

is explictly

given by induction [11, 37]. The asymptotic

expansion (17) can be integrated by part and thus give an

asymptotic expansion for  thanks to (16).

Finally, by inverting (12), we get asymptotic expansion of

the lognormal implied volatility.

thanks to (16).

Finally, by inverting (12), we get asymptotic expansion of

the lognormal implied volatility.

The stochastic differential equation for the CEV diffusion model is

Let  be the probability density function to get

state

be the probability density function to get

state  at -time

starting from at time . There is a closed form formula for in terms of the modified Bessel function

at -time

starting from at time . There is a closed form formula for in terms of the modified Bessel function  :

:

with  (in the most popular cases we have

(in the most popular cases we have  ) and

) and

|

The following well known asymptotic expansion for  is due to Hankel:

is due to Hankel:

On the other hand, Tanaka's formula shows that the time-value

of the call-price with strike

and maturity is given by

|

For short maturities , the

combination of (18) and (20) yields an

asymptotic expansion of  that can be integrated

by parts to any order with respect to .

This leads to an asymptotic expansion of the time-value

of a call price. Using an asymptotic expansion of the inverse function

of the Black-Scholes function seen in section 4.5, we

deduce an asymptotic expansion of the implied lognormal volatility of

the CEV model at any order in .

that can be integrated

by parts to any order with respect to .

This leads to an asymptotic expansion of the time-value

of a call price. Using an asymptotic expansion of the inverse function

of the Black-Scholes function seen in section 4.5, we

deduce an asymptotic expansion of the implied lognormal volatility of

the CEV model at any order in .

We did an experimental implementation of our algorithm in the  with an asymptotic expansion of the

form

with an asymptotic expansion of the

form

For  , our algorithm yields:

, our algorithm yields:

In this paper, we have presented an algorithm for calculating asymptotic expansions of functional inverses of functions that are highly tangent to identity. In particular, we obtained asymptotic expansions of the implied volatility of an option call price at any order in a model-free setting. hen, we have shown how this can be applied to the CEV model. It is envisaged to apply these techniques to more sophisticated models such as the SABR model [17]. More generally, it would be interesting to combine our approach with other algorithms for the calculation of heat kernel coefficients such as [1] to get automatic asymptotic expansion at any order of the implied volatility of option call prices for a large class of financial models [2].

I. G. Avramidi and R. Schimming. Algorithms for the Calculation of the Heat Kernel Coefficients, pages 150–162. Vieweg+Teubner Verlag, Wiesbaden, 1996.

I.G. Avramidi. Heat Kernel Method and its Applications. Birkhäuser, 2015.

S. Benaim and P. Friz. Smile asymptotics. ii. models with known moment generating functions. Journal of Applied Probability, 45(1):16–23, 2008.

H. Berestycki, I. Florent, and J. Busca. Asymptotics and calibration of local volatility models. Quantitative Finance, 2(1):61–69, 2002.

N. Bourbaki. Fonctions d'une variable réelle. Éléments de Mathématiques (Chap. 5). Hermann, 2-nd edition, 1961.

R. P. Brent and H. T. Kung.  algorithms for composition and reversion of power series. In J.

F. Traub, editor, Analytic Computational Complexity.

Pittsburg, 1975. Proc. of a symposium on analytic computational

complexity held by Carnegie-Mellon University.

algorithms for composition and reversion of power series. In J.

F. Traub, editor, Analytic Computational Complexity.

Pittsburg, 1975. Proc. of a symposium on analytic computational

complexity held by Carnegie-Mellon University.

M. Craddock and M. Grasselli. Lie symmetry methods for local volatility models. Ssrn.com/abstract=2836817, 2016.

S. De Marco, C. Hillairet, and A. Jacquier. Shapes of implied volatility with positive mass at zero. SIAM J. Finan. Math., 8(1):709–737, 2017.

J. Écalle. Introduction aux fonctions analysables et preuve constructive de la conjecture de Dulac. Hermann, collection: Actualités mathématiques, 1992.

K. Gao and R. Lee. Asymptotics of implied volatility to arbitrary order. Finance and Stochastics, 18(2):349–392, 2014.

J. Gatheral, E. P. Hsu, P. Laurence, C. Ouyang, and T.-H. Wang. Asymptotics of implied volatility in local volatility models. Mathematical Finance, 22(4):591–620, 2012.

P.K.F. Gatheral, A. Gulisashvili, A. Jacquier, and J. Teichmann. Large Deviations and Asymptotic Methods in Finance, volume 110 of Proceedings in Mathematics and Statistics. Springer-Verlag, 2015.

C. Grunspan. A note on the equivalence between the normal and the lognormal implied volatility : a model free approach. ArXiv:1112.1782, 2011.

C. Grunspan. Asymptotic expansions of the lognormal implied volatility: a model free approach. Technical Report 1112.1652, Arxiv, 2011.

D. Gruntz. On computing limits in a symbolic manipulation system. PhD thesis, E.T.H. Zürich, Switzerland, 1996.

A. Gulisashvili. Asymptotic formulas with error estimates for call pricing functions and the implied volatility at extreme strikes. SIAM J. Finan. Math., 1(1):609–641, 2010.

Kumar, D., Lesniewski, A. Hagan, P. and D. Woodward. Managing smile risk. Wilmott Magazine, pages 84–108, 2002.

G. H. Hardy. Orders of infinity. Cambridge Univ. Press, 1910.

G. H. Hardy. Properties of logarithmico-exponential functions. Proceedings of the London Mathematical Society, 10(2):54–90, 1911.

P. Henry-Labordère. A general asymptotic implied volatility for stochastic volatility models. Technical Report cond-mat/050431, Arxiv, 2005.

J. van der Hoeven. Automatic asymptotics. PhD thesis, École polytechnique, Palaiseau, France, 1997.

J. van der Hoeven. Generic asymptotic expansions. AAECC, 9(1):25–44, 1998.

J. van der Hoeven. Transseries and real differential algebra, volume 1888 of Lecture Notes in Mathematics. Springer-Verlag, 2006.

J. van der Hoeven, G. Lecerf, B. Mourrain et al. Mathemagix. 2002. http://www.mathemagix.org.

R. Lee. The moment formula for implied volatility at extreme strikes. Mathematical Finance, 14(3):469–480, 2004.

Forde M. and Jacquier A. Small-time asymptotics for an uncorrelated local-stochastic volatility model. Applied Mathematical Finance, 18(6):517–535, 2011.

O. Osajima. The asymptotic expansion formula of implied volatility for dynamic sabr model and fx hybrid model. Dx.doi.org/10.2139/ssrn.965265, 2007.

D. Richardson. Zero tests for constants in simple scientific computation. MCS, 1(1):21–37, 2007.

D. Richardson, B. Salvy, J. Shackell, and J. van der Hoeven. Expansions of exp-log functions. In Y. N. Lakhsman, editor, Proc. ISSAC '96, pages 309–313. Zürich, Switzerland, July 1996.

M. Roper and M. M. Rutkowski. On the relationship between the call price surface and the implied volatility surface close to expiry. International Journal of Theoretical and Applied Finance, 12(4):427–441, 2009.

B. Salvy. Asymptotique automatique et fonctions génératrices. PhD thesis, École Polytechnique, France, 1991.

B. Salvy and J. Shackell. Asymptotic expansions of functional inverses. In P. S. Wang, editor, Proc. ISSAC '92, pages 130–137. New York, 1992. ACM Press.

B. Salvy and J. Shackell. Symbolic asymptotics: multiseries of inverse functions. JSC, 27(6):543–563, 1999.

J. Shackell. Growth estimates for exp-log functions. JSC, 10:611–632, 1990.

J. Shackell. Symbolic asymptotics, volume 12 of Algorithms and computation in Mathematics. Springer-Verlag, 2004.

M.R. Tehranchi. Uniform bounds for black–scholes implied volatility. SIAM J. Finan. Math., 7(1):893–916, 2016.

K. Yoshida. On the fundamental solution of the parabolic equation in a Riemannian space. Osaka Mathematical Journal, 1(1), 1953.